Written with the support of Gavin van den Berg and Sam Vos.

Background

At the Tree of Life Foundation, regarding the allocation of capital with a Kingdom agenda, we feel strongly that:

-

Collective effort enables bigger strategic projects / higher level of economic influence in the target geographical area

-

Local participation and investment management is crucial to avoid pitfalls due to cultural differences, lack of oversight, etc.

With this in mind, we have done the following in South Africa:

-

Set up actively managed unitized private equity and other investment portfolios on the Donor-advised Fund (DAF) platform we offer (tol.org.za/donor-advised-fund/).

-

Set up private equity vehicles for those wishing to invest with private money rather than DAF money (not further discussed in this White Paper).

-

Facilitated local investment participation (currently the bulk of capital we manage is from South African investors) and active investment oversight via a South African registered Financial Services Provider (FSP).

Whereas we have covered our views on Collective Christian Capital and the continuum of investment approaches in previous CEF White Papers,1 this paper focuses on Impact Investment (i.e., an “Impact First” as opposed to a “Return First” investment in the referenced paper) and a specific example of investment in a social enterprise where a lack of capital was the bottleneck to growth for an otherwise extremely scalable and impactful business model.

Overview of Impact Investing and Social Enterprises

A commercial enterprise has the sole purpose of maximizing profit and shareholder return. Transcending this traditional purpose of business, a social enterprise is (broadly) defined as an entity with specific social objectives, aiming to maximize both social and economic returns. Social returns include benefits to societal welfare, environmental sustainability, and—as Kingdom-oriented investors—the advancement of the Gospel.

Social enterprises have an important role to play in bringing healing and restoration to a broken world. Having a mandate to focus on social and environmental upliftment allows social enterprises to bring about change, where normal businesses are constrained.

A growing trend of identifying the need to improve social and environmental issues is being driven globally by secular institutions. In line with the United Nation’s Sustainable Development Goals, this trend has been driven from the top-down by means of an increased awareness of ESG factors taken into consideration when allocating capital.

Impact investing is the art of allocating capital with specific social and environmental objectives in mind. It is worth noting that not all impact investments require investment into social enterprises, but these concepts are deeply intertwined.

Current Limitations of Impact Investing

Noting the benefits of social enterprises, why are there not more? As is the case in traditional business, capital is at the heart of developing a sustainable economic entity. Unfortunately, social enterprises face barriers to attracting much needed capital.2 These barriers to capital include:

-

The difficulty of social impact measurement. Converting subjective matter into a quantitative, nominal figure is further complicated by contrasting views on what constitutes impact.

-

The balancing of financial and social returns. While these two types of returns are not mutually exclusive, investors’ propensity to concede financial return for social return is further complicated by the difficulty to quantitatively measure social returns.

-

An underdeveloped impact-investment market. A shortage of scale, quality impact-investment opportunities backed up by an established track record, limits investment opportunities. As a result, limited intermediaries (brokers, consultants, fund managers, etc.) exist. This in turn creates liquidity concerns, high transaction costs, and a skew toward higher-risk investment opportunities.

As a result, attracting sufficient funding for social enterprises with the potential to bring forward substantial change is often challenging.

Our observation in the Christian investment ecosystem is that there is a high presence of social impact opportunities in Third World countries but, at the same time, a lack of capital. Furthermore, the mere addition of capital to many of these opportunities does not guarantee success—more often than not, the management needs advice in refining and focusing on the core strategy, how to successfully scale (systems & people), corporate governance, measuring and reporting capability, etc.

In the First World on the other hand, there is often significant capital available that is earmarked for impact by the owners thereof, but they often face obstacles in sourcing suitable investment opportunities, thoroughly investigating them (due diligence), as well as implementing post-investment oversight. Sadly, this often gives rise to indiscriminate impact investing with the best of intentions but disappointing results (similar to how foreign aid in the form of grants/donations often do not affect the change initially hoped for).

Impact Investment Case Study: U-Turn Retail

U-turn (www.homeless.org.za ), today a registered Public Benefit Organization / charity in South Africa, was founded in 1997 by Colleen Lewis to focus on the care of homeless people in her area of Cape Town. Colleen initially operated from her home (providing food and Bible studies), but due to the growing need and concerns from neighbors, operations moved to the St Stephens church hall in Cape Town.

In 2006, Colleen stepped aside and handed the management over to a management team led by Sam Vos. Programs included feeding programs, Bible studies, an accommodation centre where homeless people were housed, and ad hoc service delivery to address whatever the needs were of a homeless person showing up for help.

Sam, being a qualified Industrial Engineer, saw the need for a more structured process through which U-turn could help people moving off the street. Due to lack of resources, this could not be done overnight (the 2006 turnover was a mere ZAR 500k, or $35k USD at current exchange rates), but they kept gradually chipping away at it until the process of “occupational therapy combined with work opportunities” settled in 2009.

I first learned about U-turn when Sam and Jonathan Hopkins attended Triga Ventures (a cutting-edge South African Organization similar to Praxis in the U.S.) in 2019, where I have the privilege to serve (www.trigaventures.org).

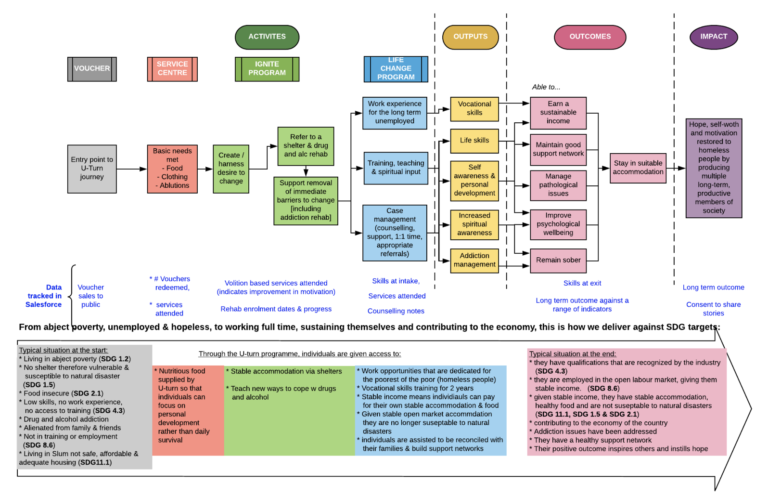

U-turn follows a holistic approach to homelessness as can be seen from Figure 1 below and is acknowledged as a thought leader with regards to this social dilemma in the local community. They recently published a well-researched paper on The Cost of Homelessness due to the combination of Humanitarian, Developmental, Reactive, and Punitive measures associated with it.3

From the above, it is evident that the provision of work and associated skills training form an important part of the overarching process that U-Turn follows. During the initial years, the government provided funding and work opportunities (e.g., cleaning up graffiti), but due to the unpredictability of these government programs, U-Turn established its first charity store in 2012. The benefit of the charity store as the employment and training component of U-turn’s program was that U-turn could be in control of their own funding as well as the length of period someone needed to be employed before moving on.

Today, they have 7 physical stores, one e-commerce store, and one laundry sorting facility—9 significant operations. Having developed and refined the IP to run these stores over a number of years, there is ample room to scale this. As part of the bigger employment ecosystem, they see the current retail operations as “but one stream of work,” and (besides significantly scaling retail operations), they have ambition to set up other things like a textile recycling plant, a recycling plant for household goods, etc.

U-Turn Retail’s shops operate like thrift shops (with the normal impact benefits of recycling secondhand goods rather than for it to end up in landfills) but with a further social and spiritual impact twist. The shops play an essential role in equipping participants, as they gain real-world work experience while earning a stipend. Ultimately, it is envisioned that participants secure an independent job in the open labor market, become active members of society, and stay off the streets. Currently, 83% of the individuals who graduate from the program remain productive members of society. (See https://youtu.be/SNW6F2061QQ and https://youtu.be/H31xUAJsmek as examples of individual testimonies).

The retail business sources second-hand goods (mainly clothes) via donations. It then sorts, cleans, and transports the goods to the retail outlets. Each of the 7 retail stores has a store manager, which oversees between 3 and 4 participants. The retail business has recently made business improvements to reinforce sustainability while employing a sub-optimal number of employees, as job-creation is their core purpose.

Currently, U-Turn Retail has the capacity for 40 rehabilitants to gain work experience. Operating in a city estimated to have 14,300 people living on the streets,3 the supply and demand relationship is sorely one-sided. To expand the rehabilitation intake, more jobs are needed. To create more jobs, growing the store network is key. While the retail business has the proven ability to sustain itself economically, its cash-flow generation is not sufficient to finance the accelerated retail expansion required to satisfy the current employment need. It is for this reason that TOL, as capital provider via our Impact First Portfolio, decided to partner with U-Turn to provide a capital solution where ordinary “Return First “capital may struggle.

To set-up a new store requires a capital expenditure of ZAR 260,000 (roughly $17k USD), with each new store creating employment for an additional store manager and 4 rehabilitants. The average monthly new store EBITDA is estimated to be roughly ZAR 8,700. To fund this expansion with external capital, a 5-year loan carrying 10% interest will require an approximate ZAR 5,700 repayment per month. The low level of cover underscores the risk associated with this investment. Investors not willing to forego the financial return adequate to compensate for the high level of risk would struggle to commit capital to U-Turn.

A ball-park interest rate figure for a justifiable risk-reward payoff in South Africa would likely be closer to 20%. For the committed impact investor, the 10% financial return differential can be justified by the creation of additional job opportunities with every store that is opened.

Since TOL provides more than capital, however, and gets actively involved in the investments we make, our expectation will be that the financial outcome at the stores may improve further. In recognition of that, we have agreed that U-Turn will pay a turnover linked fee of 7.5% to TOL but only on the turnover in the new stores and then only on the component of the turnover in excess of U-Turn’s current projections (it was furthermore agreed to cap the turnover linked fee at a 30% outperformance of turnover targets).

U-Turn Retail falls into an “Impact-First” investment bucket, with the added benefit of having a high missional rating. The business is owned by a Christian charity, run by Christian businessmen, and embedded with Christian values throughout their rehabilitation process. While subjective, TOL deems the sustainable impact opportunity a worthwhile trade-off and is willing to curtail the high return that would be required to justify the investment’s risk profile.

Our total initial investment amounts to a ZAR 1,600,000 ($107,000 USD) investment in the form of a loan to fund the setup of 6 additional retail outlets over the coming months. Our intention is that this forms the initial step in a partnership that will ultimately lead to an equity investment enabling an even more aggressive expansion of the retail platform as well as the addition of other types of businesses that can fulfill the same role.

Benefits

Investing DAF money via the Tree of Life Foundation’s (TOL) Impact Portfolio places us in the wonderful position to support sustainable businesses with explicit impact but without the level of pure financial returns that will be required for a typical private equity investment.

As mentioned, TOL offers various investment portfolios on our DAF platform. We typically seed fund these portfolios with our own balance sheet TOL funds when they are launched. Likewise, the Impact Portfolio is currently significantly funded by TOL that will dilute over time as DAF clients buy units in the Impact Portfolio, thereby also creating capacity for future transactions. Running a unitized portfolio under a DAF platform has various advantages:

-

Since there are specific portfolios with specific focus areas and benchmarks, DAF clients are clear what they are investing into and will also receive quarterly statements showing the latest value of their holding (the unit cost in each portfolio is reported quarterly).

-

It facilitates the raising of like-minded capital and the availability of capital when opportunities arise (rather than to raise funds on a transaction-by-transaction basis).

-

It facilitates transactions that are bigger than individual investors may have appetite for.

-

Each of the underlying investments is actively managed by TOL.

-

Clients spread risk across various investments in the portfolio.

-

Liquidity is possible as new DAF clients buy units in the portfolio (allowing DAF clients wishing to exit the opportunity to sell their units).

-

US investors can enjoy significant tax benefits from investing via a DAF (cross border equivalency to ensure tax benefits, although the money sits in a DAF in South Africa, facilitated by Trustbridge – trustbridgeglobal.com).

The Impact Portfolio is a relatively new addition to our value proposition (the first investment was made two years ago) but has massive potential given the abundance of such opportunities in South Africa and the growing awareness of impact investing as an alternative to grantmaking. It also complements our existing “Return First” private equity portfolio that has established a solid track record since it was launched on the DAF platform in 2016.

——

[1] Du Preez, J: Balancing Financial Returns and Impact in Private Equity Investments, CEF 2018; https://drive.google.com/file/d/1RGtgeiKdoXbGZX9PHTlqsKkBH_6tHAy6/view?usp=sharing

[2] McCallum, S.R: Private sector impact investment in water purification infrastructure in South Africa, 2018

[3] Hopkins, J, Reaper, J, Vos, S, & Brough, G: Cost of Homelessness, Cape Town, 2020.

Article originally hosted and shared with permission by The Christian Economic Forum, a global network of leaders who join together to collaborate and introduce strategic ideas for the spread of God’s economic principles and the goodness of Jesus Christ. This article was from a collection of White Papers compiled for attendees of the CEF’s Global Event.