Financial Advisor Survey 2013

The Faith Driven Investor movement stands on the shoulders of those who have come before us. John Siverling and the Christian Investment Forum are just one of the groups who have led this conversation, and we’re grateful to feature their contribution to the movement here.

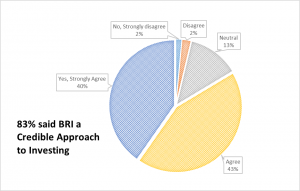

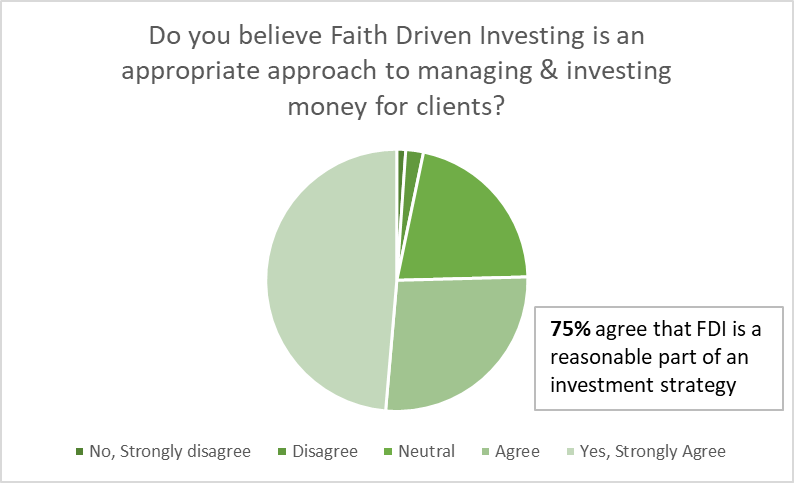

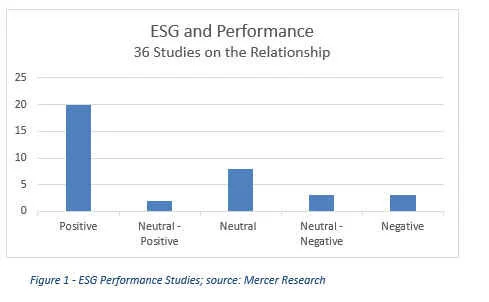

According to new survey research done by the Christian Investment Forum in 2013, the level of Biblically Responsible Investing has seen strong growth with advisors who have used BRI in their practice, with 25% of them indicating their level of BRI assets has grown by over 20% in the last year and only 4% had a decrease. This in part may be the result of the high level of interest from both advisors and investors. 80% of advisors said they would like to recommend BRI funds to their clients, and only 10% felt faith should not play a role in investing. Not only are advisors interested in BRI, but they view it as credible and comparable in performance to other investing practices.

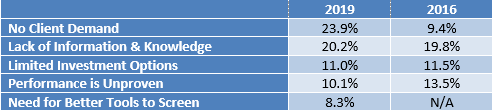

The survey also illustrated opportunities for continued growth in BRI assets. The market share of BRI assets remains significantly below what would be expected based on both investor and advisor interest. Responses from the survey suggest that knowledge of BRI, the investment choices, and the performance of BRI funds and portfolios needs to be improved in order to increase the usage of Biblically Responsible Investing.

From that survey data, following are the key takeaways:

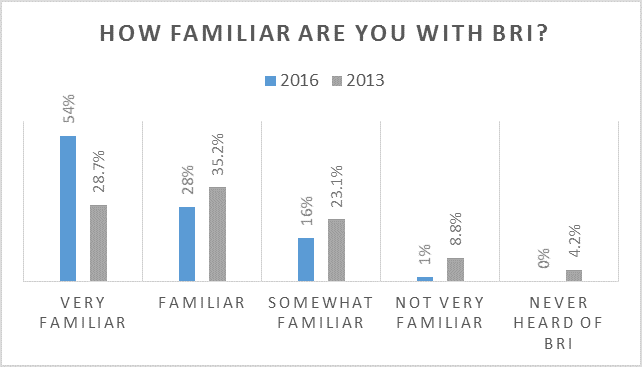

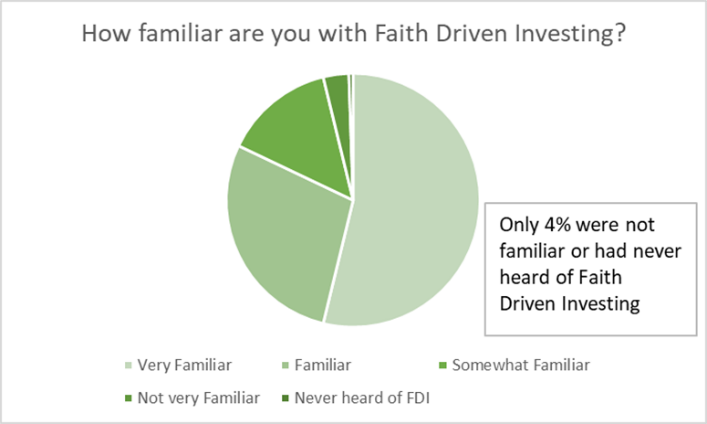

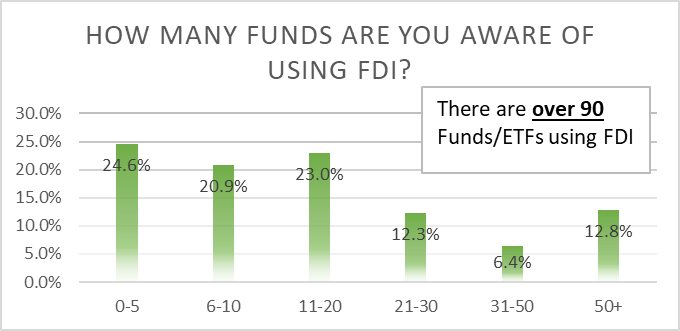

Key Takeaway #1 – Awareness is Needed

The AWARENESS of the breadth of funds that use BRI is not as high as could be expected among advisors that are pre-disposed to a faith based advisory approach, though there is a general understanding of the core features associated with Faith Based Investing.

Key Takeaway #2 – Knowledge can Improve

The level of satisfactory KNOWLEDGE in BRI lags behind the awareness of the concept with financial advisors. While they believe it is a credible approach, they seem uncomfortable to more widely implement it due to that lack of education.

Key Takeaway #3 – Usage will Follow

The USE OF BRI strategies, and investments into funds that use BRI falls significantly lower than the level the financial advisors indicated they would like, what they indicated their clients would prefer, as well as what other surveys have suggested is desired by investors.

The opportunity to fill the gap of awareness and knowledge can result in meeting a significant unmet need in the marketplace for funds and investing strategies that align with investor’s faith and values, similarly to how the socially responsible investing movement has grown.

According to the Forum for Sustainable and Responsible Investment, $3.31 Trillion of US domiciled assets were invested using SRI practices and held by 443 institutional investors and 272 money managers. Removing the institutional market from the analysis, they estimate there were 720 SRI funds with a total of just over $1.0 Trillion in assets under management in 2012. Based on a total market of $14 Trillion, SRI funds account for roughly 7% of total assets under management

The best estimates indicate there were approximately 89 religious mutual funds in 2006 with total assets of $17.7 Billion. This estimate includes all religions, including non-Christian. Research by independent wealth managers has identified approximately 50 Christian Faith Based Investing funds. Based on the interest levels expressed by both advisors and investors, and using a current low average allocation of a 10% allocation to BRI funds, the potential market for Christian Faith Based Investing is approximately $1.6 Trillion, or 100 times greater than where we are today. That suggests a long way to go but a great deal of opportunity.