Director of Faith-Based Initiatives | Calvert Impact Capital

Amanda is Director of Faith-Based Initiatives, serving as a resource for faith-based investors on their impact investing journeys. She partners with faith leaders and networks to build the capacity and community of practicing faith-based impact investors.

Prior to joining Calvert Impact Capital, Amanda worked at Opportunity Finance Network, the nation’s leading association of community development financial institutions (CDFIs) committed to providing affordable, responsible capital and financial services to communities not served by mainstream finance. There she worked with CDFI funders, investors, and practitioners as Senior Vice President, Development, and previously as Vice President, Strategic Consulting.

She has held had senior management roles at a technology company assisting Americans to sustainably move out of poverty and for a decade-plus at Jewish Funds for Justice/The Shefa Fund where she managed the first and only national initiative to organize the American Jewish community to invest in low-wealth communities across the county.

Amanda has prior experience as a commercial loan officer for the Self-Help Credit Union, and has worked with a range of mission-driven organizations. She holds an MBA from the Yale School of Management, and an AB from Bryn Mawr College.

CONTRIBUTIONS TO FAITH DRIVEN INVESTOR

Amanda Lawson is a Writer and Content Coordinator for Faith Driven Media. She is also a Research Associate in the John W Altman Institute for Entrepreneurship at Miami University in Oxford, Ohio, where she works in the L.I.F.E. (Leading the Integration of Faith and Entrepreneurship) Research Lab.

Prior to this, she completed a Master’s degree from Miami University in Foreign Relations History, during which time she was published in several academic journals. She currently serves on the Board of Directors of Living Hope Mission, a faith-based 501(c)3 in Cap Haitien, Haiti, dedicated to empowering children and families by partnering with local church leadership to develop physically, emotionally, and spiritually healthy communities.

Born and raised in Lima, Ohio, Amanda made her way to Southwest Ohio after stints in Columbus, Ohio and Herforst, Germany. She lives in a small town surrounded by corn fields and spends most of her time in the woods or the local coffee shop.

The Faith Driven Investor movement stands on the shoulders of those who have come before us. John Siverling and the Christian Investment Forum are just one of the groups who have led this conversation, and we’re grateful to feature their contribution to the movement here.

Christian faith should not be an excuse for less than our very best effort. Instead we are called to be the best we can be as we seek to glorify God in our thoughts, words and deeds. In the financial investment management field, we are stewarding God’s gifts to the clients we serve, which can bring on an extra burden to achieve competitive returns. Our ultimate scorecard of success is not the same as the rest of the world’s measuring stick, but we can make our culture better by being competitive with our performance. This can lead more investors to use their assets for human flourishing, or as Eventide Funds has taken to saying, “investing that makes the world rejoice.”

One of the ways CIF strives to build up and grow Faith Driven Investing in the public equities space is to counter the arguments used against Faith Driven Investing, such as that FDI causes underperformance, by providing both data and stories to financial advisors and investors. We love telling and reading stories about successes in the Faith Driven Investing space. Stories captivate and offer encouragement to others. What stories often lack is the empirical evidence to support the foundation of those stories. That is where our research becomes a necessity to support and defend our belief that Faith Driven Investing is not watered down investing compared to funds that don’t include faith values.

In 2015, CIF completed a study into the performance of funds using Faith based investing criteria managed by CIF members. That study provided evidence to support the position that using faith based values in the investment making process does not directly cause under-performance.

Five years later, CIF decided to re-analyze the data and extend the analysis further by looking back 15 years and comparing the averages of CIF funds with the industry averages from Morningstar. The 2020 research study on Faith based funds performance looked at all mutual funds that were managed by members of CIF, and compared the performance of those funds against the category averages over the last 15 years. The fifteen-year history allows for data from the recession of 2007-2008, the slow recovery and the long bull market we experienced until the end of 2019. Here are some highlights from the 2020 study.

Highlights

The study looked at return data for 44 Christian Faith based Funds in both equity and bond categories over a 15-year period ending December 31, 2020, and found that the performance of an average of those funds compared favorably against the benchmarks for each category, particularly in the equity funds categories. The results were consistent over different time periods of 1 year, 3 years, 5 years, 10 years and 15 years. The full 15-year period includes both bull markets and bear markets, including the 2007 – 2009 Great Recession.

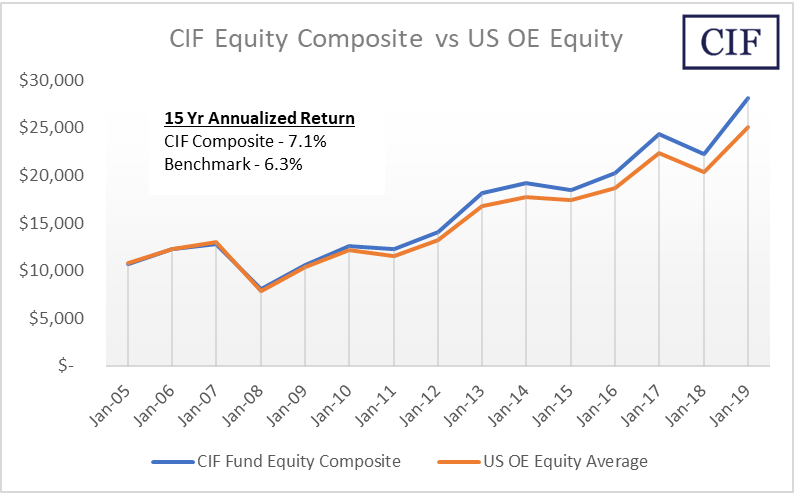

The CIF Equity Fund Composite average, with an annualized return of 7.1%, outperformed the similar Benchmark weighted average return, which had an annualized return of 6.3% over the 15-year period. There were 35 funds included in the Composite across 16 categories.

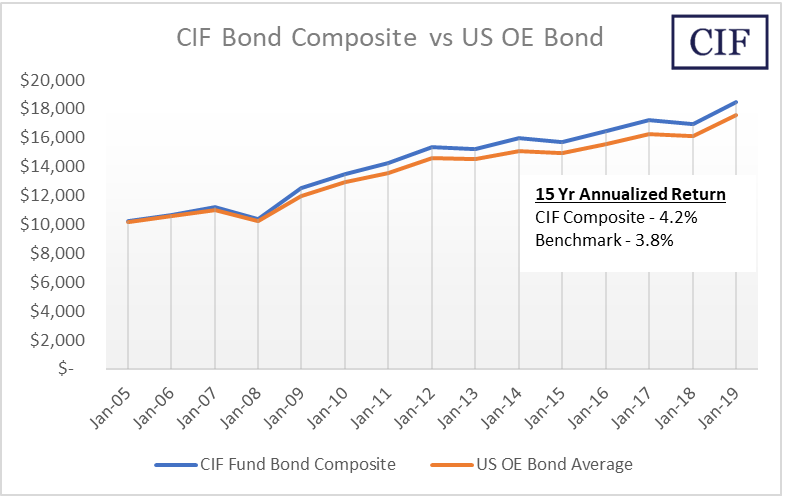

The CIF Bond Fund Composite average, with a 4.2% annualized return, outperformed the weighted average Benchmark return, which had an annualized return of 3.8% over the 15-year period.

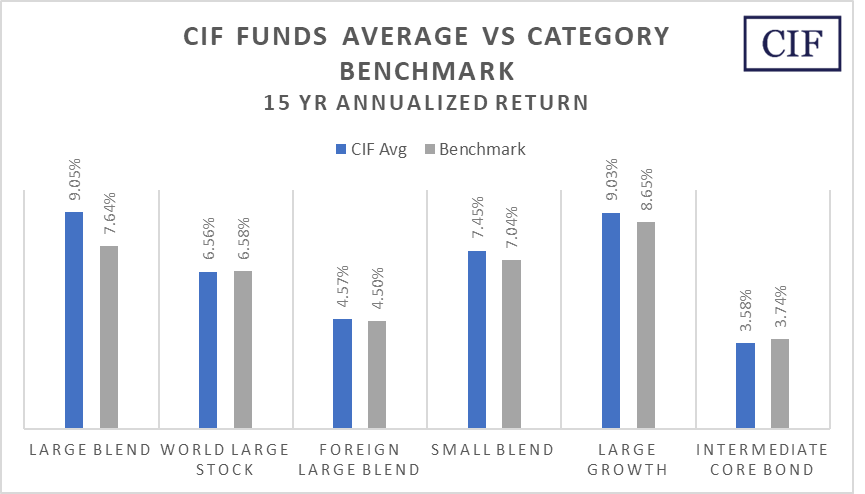

The CIF Composite, which included 9 funds in 5 categories, performed relatively equal in the 2007-2009 Recession and has slightly out-performed in the nearly 10-year bull market that ended shortly after the December 2019 end of the analysis period.

Across six categories of equity and bond funds, each of which included at least 3 funds from the CIF Funds pool, the average of those funds outperformed the category benchmark average in four of the six, and in two categories the funds averages slightly underperformed the benchmark. More analysis of the 1 year, 3 year, 5 year and 10 year time periods and risk metrics is included in the study detail.

These results support the business case that including faith based value criteria in the investment selection process can provide reasonable and competitive returns, allowing Christian investors the opportunity to invest according to their values while also acting in a financially sound manner. This dispels some of the long standing perceptions that incorporating faith based criteria in addition to traditional investment criteria is correlated to underperformance.

Author’s Note

This study collected and analyzed financial data for a 15-year period ended December 31, 2019. Given the volatility of the financial markets since February 2020 following the COVID-19 pandemic, the authors elected to review the year to date financial performance data for the CIF Funds and the related category benchmarks through May 31st, 2020 for any material or significant changes to the conclusions of this report. The 15-year annualized return for the CIF Equity Composite Average dropped to 6.5% and the Benchmark weighted average return dropped to 5.7%, but the difference between the two remained the same at 13%. Regarding the Bond category, the CIF Composite remained the same at 4.2% while the Benchmark weighted average increased to 3.8%, but again the difference remained the same at 9% outperformance for the CIF Funds Composite.

Based on this updated analysis, we do not believe the results and conclusions from the full report require any disclaimer or modification.

Originally posted on Christian Investment Forum with permission to republish

The Faith Driven Investor movement stands on the shoulders of those who have come before us. John Siverling and the Christian Investment Forum are just one of the groups who have led this conversation, and we’re grateful to feature their contribution to the movement here.

The Christian Investment Forum completed a study on BRI Funds performance to further advance the knowledge of the correlation of values based investing and investment return. The purpose of this study is to review the performance of the mutual funds managed by member firms of the Christian Investment Forum (CIF) over time relative to their respective Morningstar categories. This study is not meant to identify or rate individual mutual funds or managers, or their unique approaches to Christian faith based investing (frequently described as Biblically responsible investing, or BRI). Instead, the study seeks to analyze the broader relationship between performance and the use of BRI criteria in the investment decision making process. It is the hope of the Christian Investment Forum that others may follow with additional academic research in this specific area of investing.

The use of Biblically responsible investing by CIF Members varies in the methods used and the priorities placed on each of the foundational aspects of BRI – Screening, Governance, and Advocacy. Some firms and asset managers focus mostly on exclusionary screens of the investment pool, while others use both exclusionary and inclusionary screening. Some firms also place a priority and focus on governance issues and shareholder engagement in addition to screening.

Previous research from other firms has shown that incorporating screens for social, environmental, and governance issues has a positive relationship to performance – said another way, funds that incorporate screening on average slightly outperform the market. A review of four of these research documents is included in this paper in a following section.

These cited research studies focused largely on socially responsible investing (SRI) funds and their performance relationship to the industry averages. Socially responsible investing criteria are similar to those used by faith based funds, and in fact the SRI databases usually include faith based funds in the universe studied. Thus it is reasonable to view the findings of these studies as good proxies for the performance of faith based funds relative to the industry, but the direct relationship between faith based funds and performance may be hidden within the larger universe studied.

This study by the Christian Investment Forum focused only on Christian values based investing and the funds that follow this approach. The goal was to test if this smaller segment of the broader socially responsible investing market had the same positive relationship to performance.

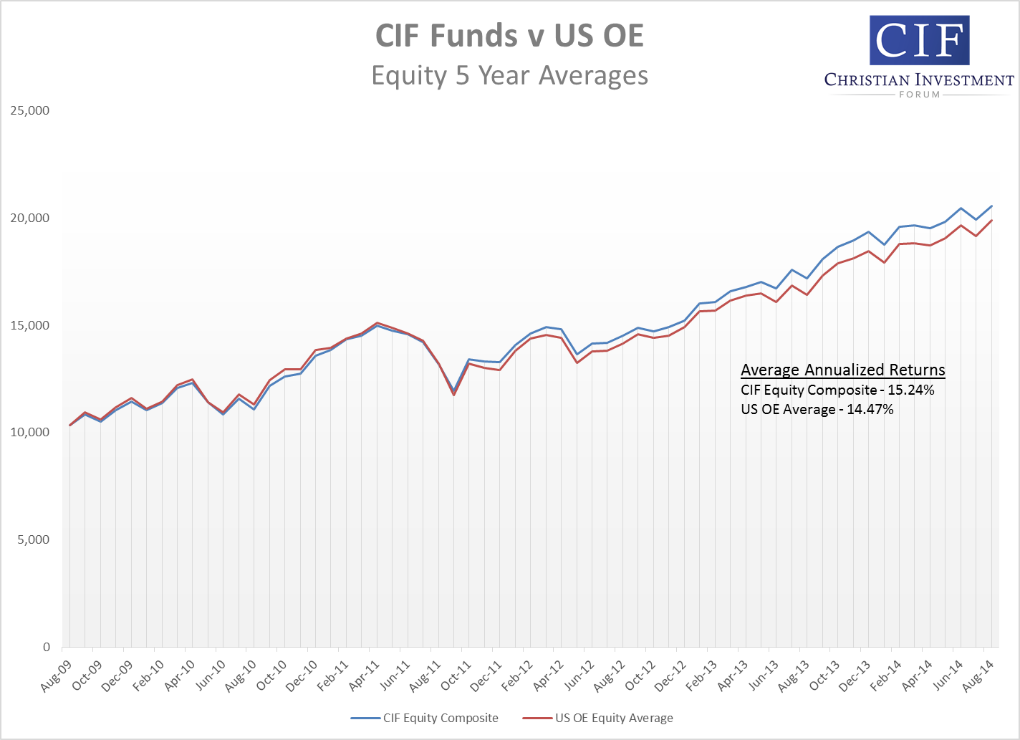

Based on the analysis of historical performance data from the funds managed by members of the Christian Investment Forum, the results did in fact corroborate the expectation that return performance was not reduced due to incorporating BRI, and in fact there was a general outperformance compared to the industry averages. Over the last 5 years, a composite of the returns from all of the equity mutual funds within the Christian Investment Forum outperformed the industry average by 77 basis points (bp) on an annualized basis.

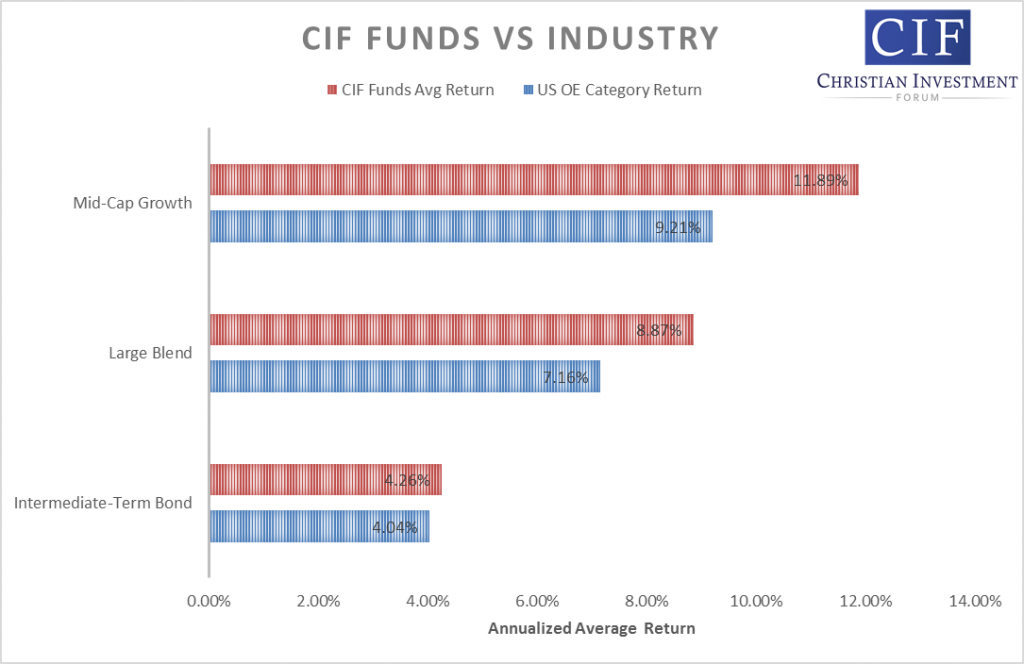

This broad equity composite is an easy summary to communicate, but it lacks the specificity of individual asset classes that is more valuable for analysis and for actual implementation. Looking closer at specific categories, similar results were shown. Categories were chosen which had at least 4 CIF funds in order to reduce individual fund overweighting of results. In the Mid-Cap Growth category, the CIF funds composite outperformed the industry average 11.89% versus 9.21% on an annualized average return basis. For the Large Blend category, the CIF Funds had a composite return of 8.87% compared to the average of 7.16%. In the Intermediate-Term Bond category, the returns were very close, with a slight edge to the CIF Fund composite – 4.26% to 4.04% for the industry average.

Following the review of other Academic Research, we provide the details of the results for each asset class listed in the above chart – Mid-Cap Growth, Large Blend, and Intermediate-Term Bond.

In conclusion, the results of the prior research and this study of funds from CIF Member Firms reinforces what has been communicated by CIF on the advantages of BRI and the competitive performance of portfolio managers from firms in the Christian Investment Forum. More research is warranted to further what has been done to date, and as longer time periods become available to analyze. As is frequently pointed out, historical results are not predictive of future performance. This is also true for perceptions or expectations of under-performance for BRI funds based on some prior experience. With this study and others, we hope to re-engage with investors and advisors so they can review the current performance results of these BRI funds relative to the industry.

The results of this analysis are not meant to suggest that BRI funds will result in outperformance. The most important reason to incorporate BRI funds into an overall investment portfolio is to better align investments with an investor’s values. For investors and their advisors, considering funds that can align with their Christian faith need not be a choice between values and performance.

Link to Review of Academic Studies

The Faith Driven Investor movement stands on the shoulders of those who have come before us. John Siverling and the Christian Investment Forum are just one of the groups who have led this conversation, and we’re grateful to feature their contribution to the movement here.

When we look beyond the socially constructed and restrictive barriers of race, class, faith, and gender, we may at first see the stranger, then we recognize our neighbor, and verily, we also see ourselves.